Money, Inflation, and Rising Prices: What Are the Risks for the Short-term Outlook?

Col. E.C. Harwood, AIER’s founder, was a staunch defender of the gold standard and a harsh critic of fiat money, or money that the government declares is legal tender. He understood the dangers of allowing monetary authorities unbridled influence over the nation’s money. At no time in our nation’s history are those concerns more relevant than now.

Following the Great Recession, the Federal Reserve undertook several initiatives to stimulate the economy through monetary policy. The Fed lowered its target short-term interest rate, the fed funds target, essentially to zero. When that failed to produce the desired results, the Fed engaged in several programs known as quantitative easing. These programs were intended to ease credit conditions in the broader economy by rapidly expanding the quantity of reserves held at the Fed by commercial banks. Seven years after the end of the Great Recession, the results of those programs pose a potential risk to the general price level.

The Fed’s balance sheet shows total assets of $4.5 trillion, with $4.2 trillion of securities held directly. Of that $4.2 trillion, $2.5 trillion is held in Treasury securities and $1.7 trillion is in mortgage-backed securities. Those holdings are a result of the quantitative-easing programs implemented during and after the financial crisis.

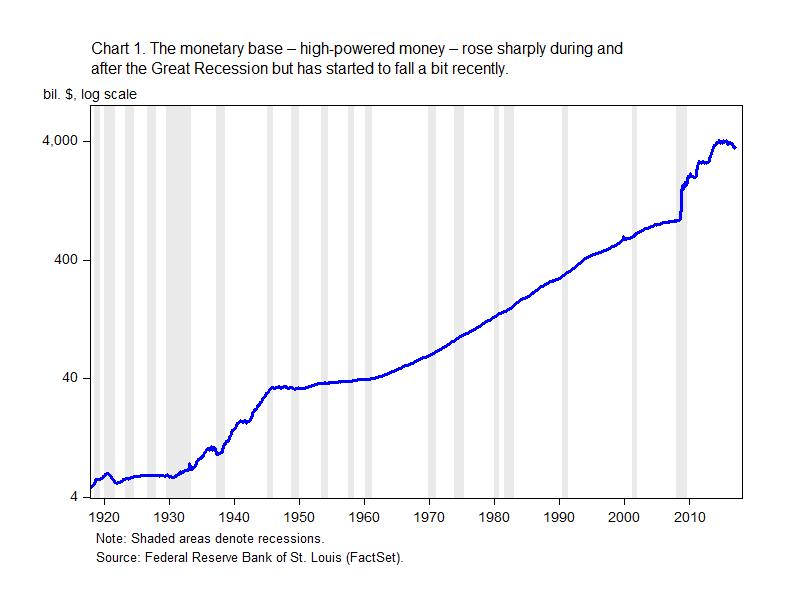

On the other side of the ledger, commercial bank reserves held at the Fed have ballooned to $2.1 trillion, of which about $133 billion is required reserves and the remaining $2 trillion is excess reserves held above the required amount. Add to those reserves about $1.5 trillion of currency in circulation, and the U.S. economy has a monetary base of $3.6 trillion (Chart 1). To a monetarist, those are extremely frightening numbers.

Monetary theory shows that inflation, meaning a broad decline in the purchasing power of money (not to be confused with changes in relative prices) is always the result of a mismatch between money demand and money supply. Create too much money and purchasing power declines. With a monetary base (also known as high-powered money) of $3.6 trillion, the potential for a surge in money supply, and therefore in inflation, cannot be ignored.

For reserves to have an impact on monetary aggregates, the banking system needs to make loans. Those loans are then used for things like consumption or business capital investment, eventually ending up back in the banking system as deposits and increasing the money supply. If the new demand created by the loans exceeds the current money supply, then prices tend to rise.

While the gargantuan pile of reserves held at the Fed represents an enormous risk to price stability, there are offsets that should keep even monetarists from complete panic. First, the Fed has new tools (their newness means limited real-world experience with their effectiveness), such as paying interest on excess reserves, which is intended to help restrain growth in the money supply. By paying interest, the Fed provides an incentive for banks to refrain from making loans to the public. The rate the Fed pays on excess reserves also serves to influence the rate banks will charge on loans made to consumers and businesses. The Fed can also begin to sell its holdings of securities to directly reduce excess reserves.

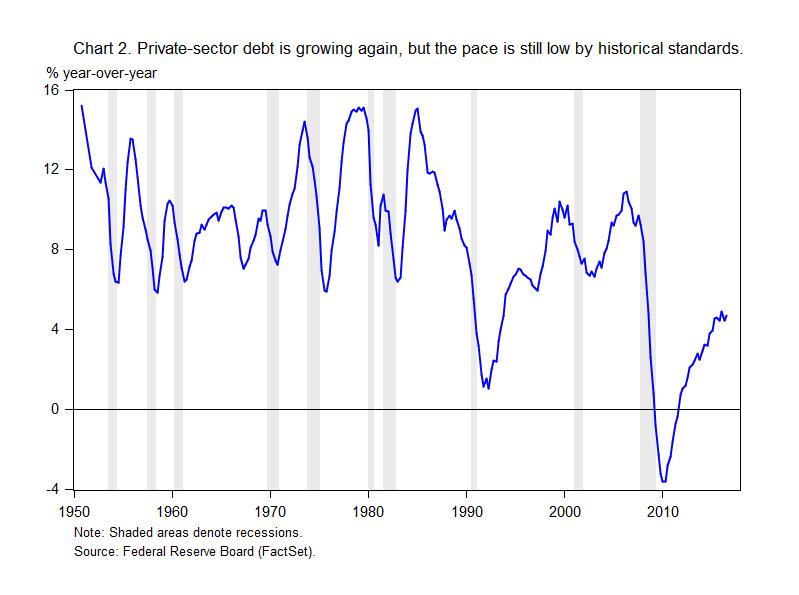

Second, though a massive amount of excess reserves remains on deposit with the Fed, loan demand and loan creation during much of the current economic expansion has been moderate. Private nonfinancial- sector debt, meaning consumer and business debt, has been growing just below 5 percent recently, but so far, that pace remains below the typical historical rates of 5 to 10 percent a year (Chart 2).

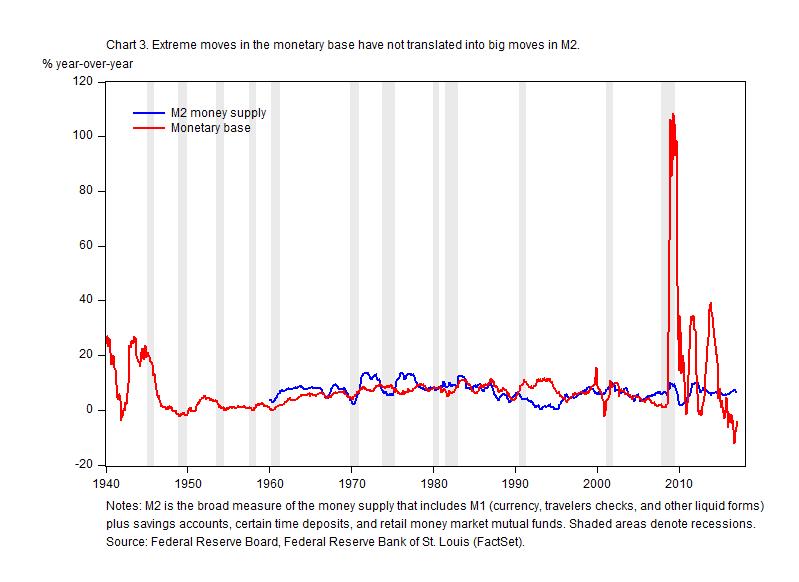

Without corresponding loan growth, the transmission mechanism for reserves and the monetary base to become money in circulation is disabled. Despite the huge surge in the monetary base during and following the Great Recession, the M2 money supply has grown at a pace roughly in line with the past 30 years (Chart 3). M2 money is up just under 8 percent over the past year, in the upper half of the 0 to 10 percent per year growth the M2 has posted over the past three decades. In addition, just as debt creation has begun to accelerate over the past year or so, the monetary base has begun to shrink, though the amount of excess reserves remains enormous.

It should also be noted that in the short term, many things can offset or distort the influence of monetary growth on prices. Swings in the supply and demand of commodities, changes in labor costs and productivity, movement in the exchange rate of the dollar, or changes in the supply and demand for final goods or services may affect relative prices in the short term. And the impact of these forces on short-term relative price moves can be hard to distinguish from true inflation that results from excess money creation.

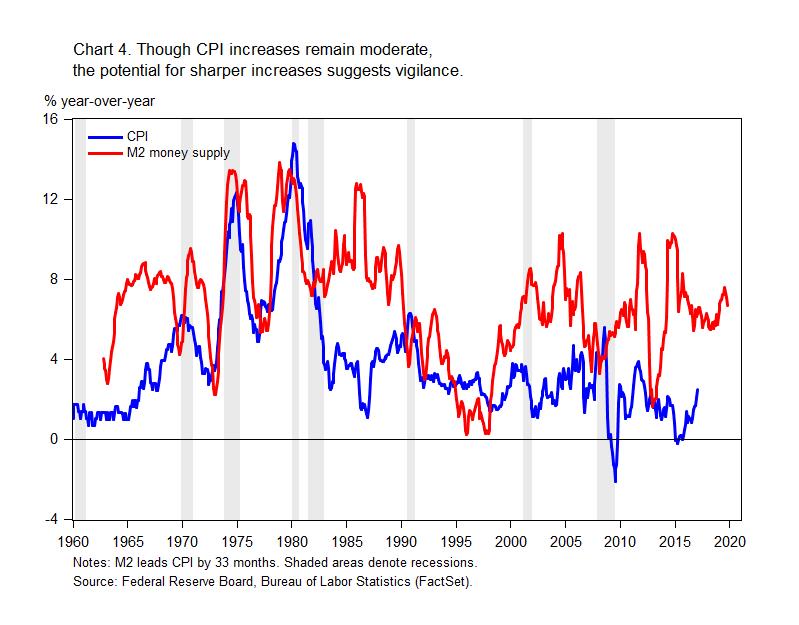

Still, in the long run, only excess money supply can result in increases in the general price level and declines in purchasing power. Over the past six decades, there has been just under a three-year lead between M2 money growth and changes in the Consumer Price Index (Chart 4). Given that lead, there is plenty of reason to be concerned by the enormous level of reserves held by commercial banks at the Fed, despite slow debt growth and more recent declines in excess reserves.

Given all these concurrent forces, the prudent behavior is to be diligent in tracking activity in the U.S. economy. Changes to policy and developments in the growth of all the measures of money and credit are critical drivers of economic activity and prices. For now, economic activity appears to be accelerating and price increases remain moderate, but risks to both remain.

Robert Hughes

Robert Hughes joined AIER in 2013 following more than 25 years in economic and financial markets research on Wall Street. Bob was formerly the head of Global Equity Strategy for Brown Brothers Harriman, where he developed equity investment strategy combining top-down macro analysis with bottom-up fundamentals. Prior to BBH, Bob was a Senior Equity Strategist for State Street Global Markets, Senior Economic Strategist with Prudential Equity Group and Senior Economist and Financial Markets Analyst for Citicorp Investment Services. Bob has a MA in economics from Fordham University and a BS in business from Lehigh University.