Prices Decline in May, Monetary Policy Tightens

The United States experienced a mild deflation in May, according to new data from the Bureau of Economic Analysis (BEA). The Personal Consumption Expenditures Price Index (PCEPI), which is the Federal Reserve’s preferred measure of inflation, grew at a continuously compounding annual rate of -0.1 percent in May 2024, down from 3.2 percent in the prior month. The PCEPI has grown 2.5 percent over the last year and 3.8 percent per year since January 2020, just prior to the pandemic. Prices today are 8.9 percentage points higher than they would have been had the Fed hit its 2-percent inflation target over the period.

Core inflation, which excludes volatile food and energy prices, has also declined. Core PCEPI grew at a continuously compounding annual rate of 1.0 percent in May 2024, down from 3.1 percent in April and 4.0 percent in March. Core PCEPI has grown 2.5 percent over the last year and 3.6 percent per year since January 2020.

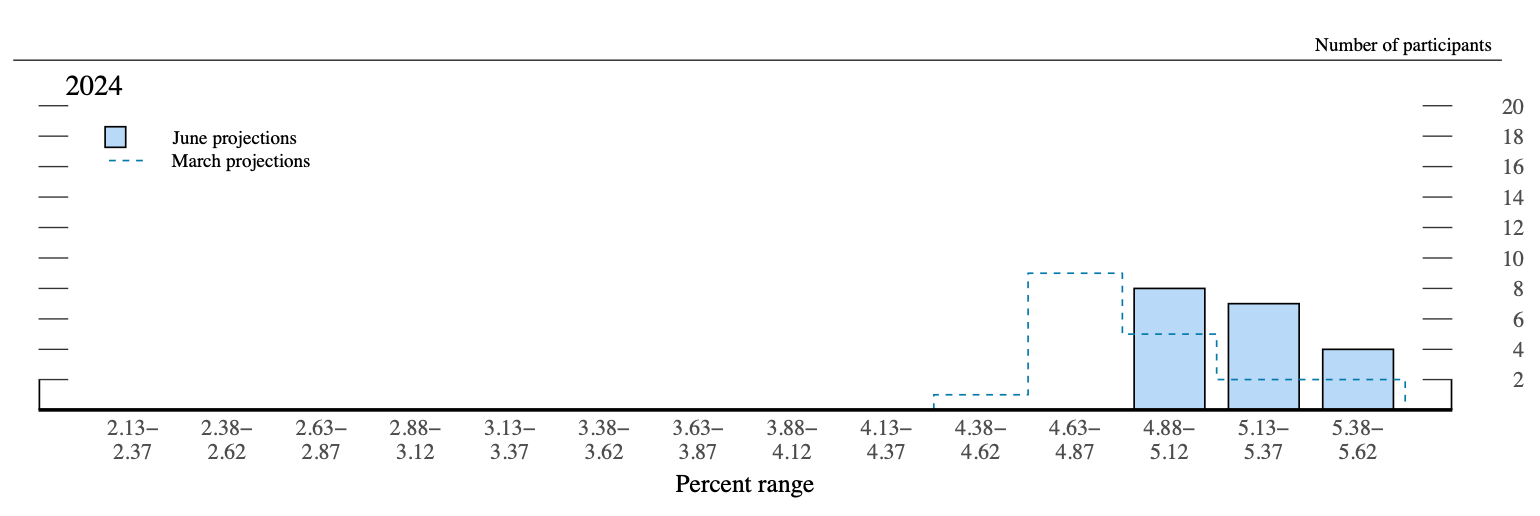

Earlier this month, members of the Federal Open Market Committee (FOMC) suggested the federal funds rate target range would need to remain at 5.25 to 5.5 percent for longer than had previously been thought. The median FOMC member projected just one 25-basis point rate cut this year, down from three projected back in March. Eight members projected two cuts. Seven members projected one cut. Four members projected zero cuts.

The latest inflation numbers bolster the case for lowering the federal funds rate target. As inflation declines, the real (inflation-adjusted) federal funds rate target increases. To prevent the real interest rate from rising, and monetary policy from tightening even further, the FOMC must lower its nominal federal funds rate target.

A numerical example serves to illustrate. Recall that i = r + E(ᴨ), where i is the nominal federal funds rate target, r is the real federal funds rate target, and E(ᴨ) is expected inflation. Suppose one uses the prior month’s core PCEPI inflation reading as a proxy for E(ᴨ). With core inflation at 3.1 percent, as it was two months ago, the Fed’s nominal target range of 5.25 to 5.5 percent implies a real target range of 2.15 to 2.4 percent. With core inflation at just 1.0 percent, as it was last month, the implied real target range is 4.25 to 4.5 percent. The FOMC would need to cut its nominal federal funds rate target by 2.1 percentage points just to leave the real target range unchanged.

While illustrative, the numerical example admittedly oversimplifies the problem. The FOMC doesn’t really know how much inflation expectations have declined nor how much it would need to adjust its nominal federal funds rate target range to prevent the real target range from rising. Still, the direction of the change required by the numerical example seems correct. When the FOMC set the current target range in July 2023, the PCEPI was growing 3.3 percent year-on-year. Core PCEPI was growing 4.1 percent. Both of those rates have since declined to 2.5 percent. Inflation is 0.8 to 1.6 percentage points lower, but the federal funds rate target range is unchanged.

Of course, what ultimately matters for judging the stance of monetary policy is not the level of the real federal funds rate but rather the difference between the real federal funds rate and the so-called natural rate, r*. If r > r*, monetary policy is tight. If r = r*, monetary policy is neutral. If r < r*, monetary policy is loose.

We do not observe r*, but the New York Fed estimates it was 0.83 to 1.34 in 2023:Q2. In 2024:Q1, the latest quarter for which data is available, it was estimated at 0.7 to 1.18. Hence, the natural rate of interest is thought to have declined 0.13 to 0.16 percentage points in the time since the FOMC set its current target range, which — on its own — would increase the spread between the real federal funds rate and the corresponding natural rate, thereby tightening policy.

Falling inflation likely means that the implied real federal funds rate target range has increased over the last eleven months. Estimates of the natural rate have also declined. Together, lower inflation and a lower natural rate of interest imply that the spread between the natural rate and the implied real federal funds rate target has grown. In other words, monetary policy has gotten tightener. Given the progress made on inflation and the current stance of monetary policy, it makes sense for the Fed to begin cutting its federal funds rate target. It must return policy to neutral, to avoid putting the economy in reverse.

William J. Luther

William J. Luther is the Director of AIER’s Sound Money Project and an Associate Professor of Economics at Florida Atlantic University. His research focuses primarily on questions of currency acceptance. He has published articles in leading scholarly journals, including Journal of Economic Behavior & Organization, Economic Inquiry, Journal of Institutional Economics, Public Choice, and Quarterly Review of Economics and Finance. His popular writings have appeared in The Economist, Forbes, and U.S. News & World Report. His work has been featured by major media outlets, including NPR, Wall Street Journal, The Guardian, TIME Magazine, National Review, Fox Nation, and VICE News. Luther earned his M.A. and Ph.D. in Economics at George Mason University and his B.A. in Economics at Capital University. He was an AIER Summer Fellowship Program participant in 2010 and 2011.