Easy Money Talks

By pumping more cash into the banking system, the Fed aims to encourage banks to make more loans. This would spur borrowing, spending, and investment, thus accelerating economic activity.

This policy may improve the economy in the short term, and it clearly helps the stock market. But two problems limit the strategy’s effectiveness.

While the Fed can increase the money supply, it has little control over where the money will go. Even if the policy succeeds in giving the recovery a boost, the borrowing it promotes may set us up for trouble down the line.

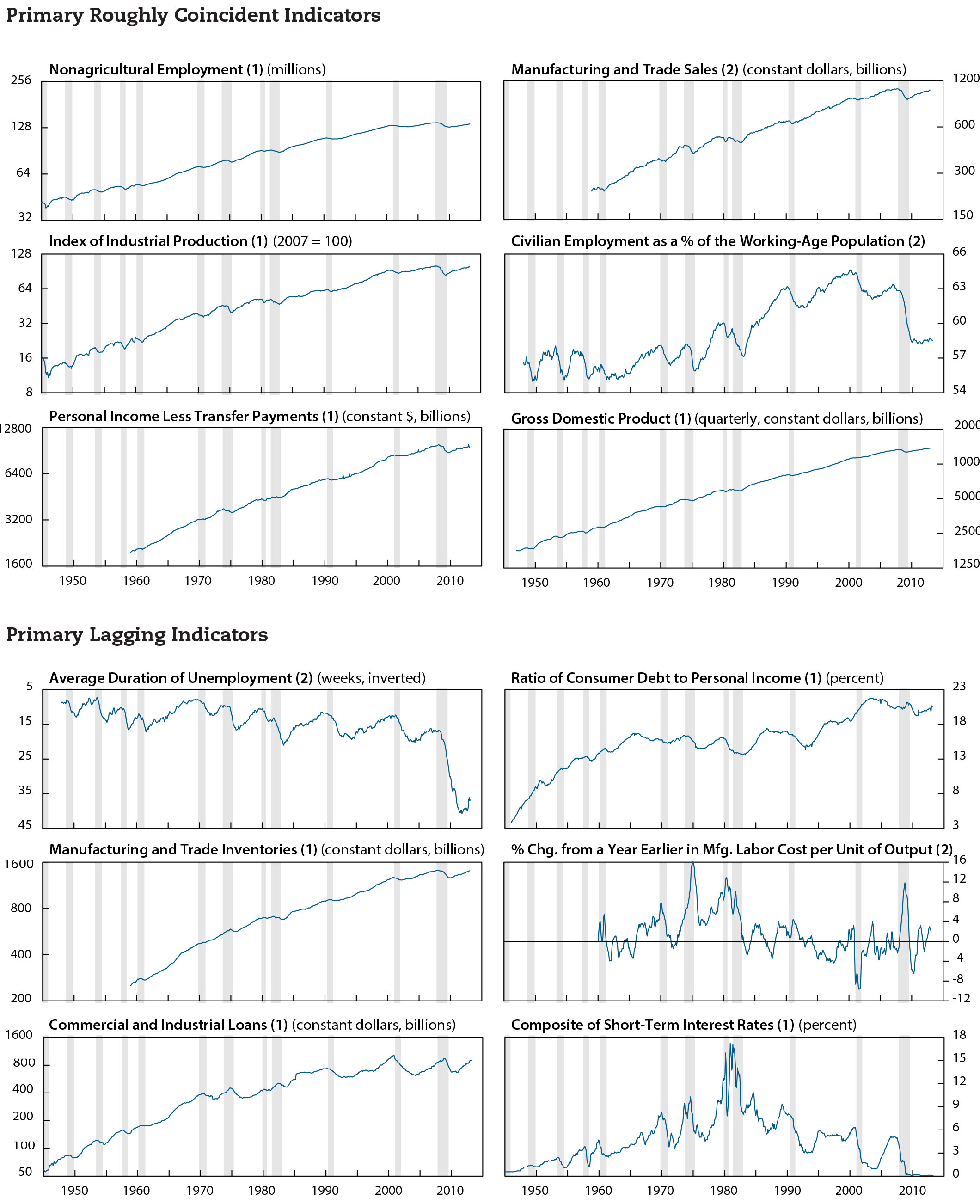

Right now, the recovery looks solid. AIER’s indicators of business-cycle conditions point to a continued expansion. All of our primary leading indicators for which a trend is apparent are trending upward, as was true last month. The cyclical score of leaders, which is based on a separate mathematical analysis, remains unchanged at 84. For both measures, a value above 50 implies that continued expansion is likely.

Our economists also find that 100 percent of coincident indicators and 100 percent of lagging indicators are expanding, confirming that the recovery has been underway for some time.

One feature that stands out in the data is a substantial acceleration in the growth of the money supply since late last year. Among the leading indicators, this is captured most directly by the M1 money supply, which increased 11 percent (adjusted for inflation) over the past 12 months.

The acceleration of money growth came primarily as a result of the Federal Reserve’s decision to purchase additional mortgage-backed securities and Treasury securities. In September 2012, the Federal Open Market Committee, the policymaking body of the Fed, announced purchases of mortgage-backed securities at a pace of $40 billion a month. In December, the FOMC announced that the Fed would also start purchasing Treasury securities at a pace of $45 billion a month.

These purchases continue to this day. Of the $530 billion of assets the Fed has added to its balance sheet since September, about $215 billion came in the form of Treasury securities and $305 billion in the form of mortgage-backed securities. (See Chart 1 on page 4.) Total assets on the Fed’s balance sheet stand at about $3.3 trillion—over three times the level prior to the onset of the financial crisis in 2008.

The Fed’s decision to engage in additional monetary easing was prompted by a slowdown in economic growth. In the second quarter of 2012, GDP growth dropped to a 1.3 percent annual rate, down from 2 percent the previous quarter and 4 percent the quarter before that.

At the same time, employment growth fell to about 100,000 jobs per month, down from a monthly pace of about 250,000 new jobs. The unemployment rate stalled at 8.2 percent. Faced with these data, the Fed concluded that the economy needed additional stimulus.

A similar scenario arose toward the end of 2012. GDP growth in the fourth quarter slowed almost to a halt. The early estimate put it at -0.1 percent, but the revised value, which incorporated more complete data, came to a 0.4 percent annual rate. This was considerably below the previous quarter’s 3.1 percent growth.

Even though the economy continued to add jobs at a decent rate of about 200,000 per month, the slowdown in output evidently worried the Fed enough to prompt it to engage in additional easing via purchases of Treasury securities.

Since then, economic growth has accelerated. In the first quarter of 2013, GDP grew at an annual rate of 2.4 percent. The economy continues to add jobs at a rate of about 200,000 jobs a month, and the unemployment rate dropped from 7.9 percent in January to 7.5 percent in April before inching up to 7.6 percent in May.

But there is no way to tell how much of the resumed growth resulted from the Fed’s asset purchases. Unlike physicists, economists cannot conduct controlled experiments to see what would have happened under different policy scenarios. It is possible that the growth would have picked up without any actions by the Fed. Improved consumer sentiment, as well as an end to the fiscal impasse in Washington, gave businesses reason to expand output, and the improved outlook in Europe put less strain on American exports.

While we cannot tell how much of the current growth was stimulated by the Fed, the data can tell us where the money they were trying to free up went. Most of it simply settled at the banks.

Excess reserves, which are essentially the cash banks hold over and above the quantity needed to meet day-to-day withdrawals, have increased almost in lockstep with the Fed’s asset purchases. Of the $530 billion the Fed has added to its balance sheet since September, about $360 billion stayed in banks as excess reserves. (See Chart 2 on page 4.) This money is not being loaned, so it does not create any additional economic activity.

However, a much smaller amount of money has been loaned. Recent data confirm an increase in borrowing by businesses and consumers.

Business borrowing in the form of commercial and industrial loans, one of our lagging indicators, has been on an upward trend for two years. In recent months, growth in these types of loans has accelerated. Since September 2012, when the Fed introduced the new asset purchases, commercial and industrial loans grew by $60 billion to a total of $900 billion (adjusted for inflation). They have now surpassed the level reached prior to the onset the financial crisis in 2008.

Consumer borrowing is also on the rise. Since September 2012, consumer credit outstanding, which includes car loans, credit card balances, student loans, and store credit, but excludes mortgages and home equity loans, has grown by 3.1 percent. This is reflected in the change in consumer debt, one of our leading indicators, and corresponds to an annual growth rate of about 6.2 percent. The last time consumer debt increased this fast was in the middle of 2007, shortly before the recession hit.

Moreover, consumer debt is growing faster than income. The ratio of consumer debt to personal income, a lagging indicator, has returned to its pre-recession high, hovering around 20.6 percent.

These trends are confirmed by the Federal Reserve’s most recent Senior Loan Officer Survey on Bank Lending Practices.

The surveyed banks report that, over the three months to April, demand for commercial and industrial loans, commercial real estate loans, residential mortgages, and auto and credit card loans increased. In response to rising demand and competition, many banks are easing credit terms on commercial and industrial loans. Banks also report that they are more willing to make consumer installment loans, but they are not easing credit standards much.

All this suggests that the Fed’s security purchases made people and businesses more willing to borrow and banks somewhat more willing to lend.

The additional money flowing through the economy has started to push up asset prices. Since December, the S&P 500 index of common stock prices, one of our leading indicators, rose 9 percent (adjusted for inflation). House prices are also on a steady upward trend.

These are among the effects the Fed sought to produce with its policy. Rising house and stock prices make people feel richer, which may induce them to increase spending. Economists call this “the wealth effect.” The size of this effect is debatable, but it probably produced some increase in spending in recent months. Inflated house prices also help homeowners who are underwater on their mortgages.

Our business-cycle indicators suggest that the real economy—the part concerned with producing goods and services, as opposed to moving money around—may be responding to the recent increase in borrowing and spending.

Among the leading indicators, rising new orders for consumer goods imply that businesses are stocking up on consumer goods because they expect higher demand going forward. Similarly, expanding new orders for core capital goods suggest that businesses are considering increasing their productive capacity. New housing permits are also rising, responding to the revival in the housing market.

Among the coinciders, the index of industrial production, manufacturing and trade sales, and GDP all continue their upward trend, reflecting increasing production and sales.

But the Fed’s policy also creates risks down the road. Easy money and record low interest rates create incentives for everybody to borrow—possibly more than is prudent.

At this point, people have as much consumer debt relative to income as they did at the onset of the financial crisis. Businesses are also back to their pre-recession borrowing levels for commercial and industrial loans.

In essence, the Fed’s easy money has encouraged everyone to be a borrower. Companies are taking out loans. People are taking out mortgages and credit cards.

At the same time, the Fed’s purchases of Treasury securities and historically low Treasury yields have made it much easier for the federal government to finance budget deficits, allowing Congress to avoid politically unpopular steps required to put federal fiscal matters on a sustainable long-term path.

The Fed is likely to face political pressure to keep interest rates low. If the federal government as well as the majority of people and businesses are net borrowers, they will all prefer rising inflation to rising interest rates. Inflation benefits borrowers by eating away at the real value of outstanding debt.

In a nation of borrowers, when the Fed has to decide between accelerating inflation and rising interest rates, which will it choose?

[pdf-embedder url=”https://www.aier.org/wp-content/uploads/2014/01/BCC20130601.pdf“]