In a recent article, I described how the Fed influences the federal funds rate in a corridor system. But, as I noted there, we are not in a corridor system. The federal funds rate (FFR) is currently below the interest the Fed pays banks to hold reserves. And that, as George Selgin explains in his forthcoming book, makes all the difference.

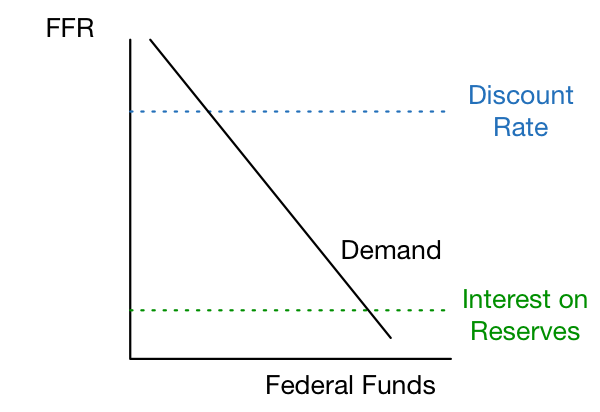

Figure 1.

Let’s start by considering the demand curve discussed in the earlier article and depicted in figure 1. Recall that the demand curve reflects private financial institutions’ willingness to hold federal funds at alternative federal funds rates. Next, consider the demand for federal funds at federal funds rates above the prevailing discount rate. Over this range, banks can acquire federal funds directly from the Fed’s discount window at a rate lower than they would have to pay other banks. Hence, the demand curve depicted in figure 1 is non-binding when the FFR exceeds the discount rate. In practice, it might be a bit more complicated. If there is a stigma attached to discount-window borrowing, banks might be willing to pay a premium to borrow from other banks. Still, the discount rate creates an upper bound (i.e., the discount rate plus the premium) on the rate banks will pay other banks to borrow federal funds.

Next, consider the demand for federal funds at rates below the prevailing interest on reserves. Over this range, banks earn more interest from the Fed by holding federal funds than they would from lending those funds to other banks. Hence, the demand curve depicted in figure 1 is non-binding when the FFR falls below the interest the Fed pays on reserves. In practice, it might be a bit more complicated. If a financial institution is ineligible for the interest the Fed pays, it might lend its federal funds to banks eligible for the interest at a rate somewhat lower than what those banks could receive from the Fed. In this case, the ineligible financial institution earns a higher interest rate from the borrowing bank than it would receive if the Fed were not paying interest on reserves and the borrowing bank captures the spread between what the Fed pays and the ineligible institution accepts. Still, the interest rate on reserves creates a lower bound on the rate banks will pay other banks to borrow federal funds (i.e., the interest on reserves minus the spread earned by banks borrowing from ineligible financial institutions).

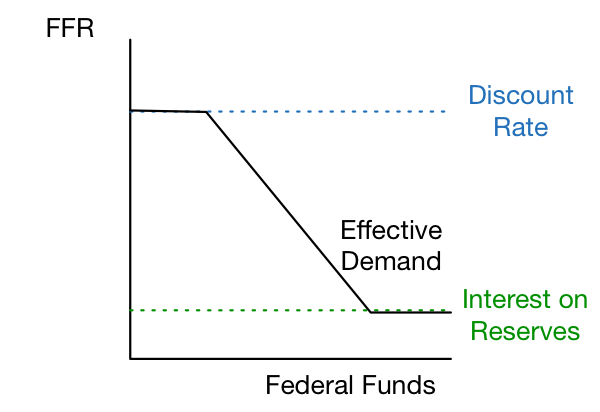

Taking into account the non-binding portions of the demand curve in figure 1 and ignoring the minor complications discussed above, we can draw an effective demand curve for federal funds given the prevailing discount rate and interest on reserves as in figure 2.

Figure 2.

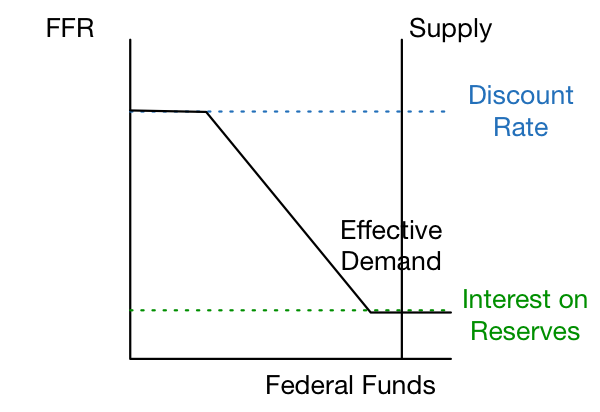

Next, consider the effectiveness of open-market operations when the Fed is operating in a floor system. For the Fed to be operating in a floor system, the supply of reserves must be so large that the prevailing FFR is at the interest paid on reserves. This scenario is depicted in figure 3.

Figure 3.

We can see now that asset purchases, which increase the supply of federal funds, will not reduce the FFR in a floor system. Similarly, asset sales, which decrease the supply of federal funds, will not increase the federal funds rate so long as those asset sales are not sufficient to return the Fed to a corridor system. Hence, the supply of federal funds has no effect on the FFR so long as the Fed is operating in a floor system.

To affect the federal funds rate in a floor system, the Fed cannot rely on open-market operations. Instead, it must adjust the interest rate it pays on reserves. If it increases the rate it pays on reserves, the federal funds rate will also increase as a larger portion of the demand curve becomes non-binding. Similarly, if it decreases the rate it pays on reserves, the federal funds rate will decrease as a larger portion of the demand curve becomes binding. Hence, the Fed must abandon its traditional policy lever — open-market operations — in favor of managing the interest it pays on reserves if it is to hit its FFR target while operating in a floor system.

In my next article, I will discuss how the Fed transitioned from a corridor to a floor system, and the somewhat puzzling policy steps that followed.