In a recent article, William Luther notes that the theoretical price level is just a numeraire, without significant implications; that relative prices, whatever the price level is, are what matter for resource allocations; but that, in practice, measured price levels do not capture all prices. Therefore, he argues that price levels can convey information about changes in relative prices in some instances.

As an example, consider the consumer price index and the producer price index. An important difference between these two indices is that the latter includes prices of intermediate goods. Consider a scenario in which increases in productivity should produce a benign deflation as measured by the consumer price index. A central bank committed to price-level stability would resist this benign deflation and loosen its monetary policy such that the price level remains constant. This is the case of implicit inflation, where the excess of money supply manifests itself as preventing a price level from falling rather than letting it increase.

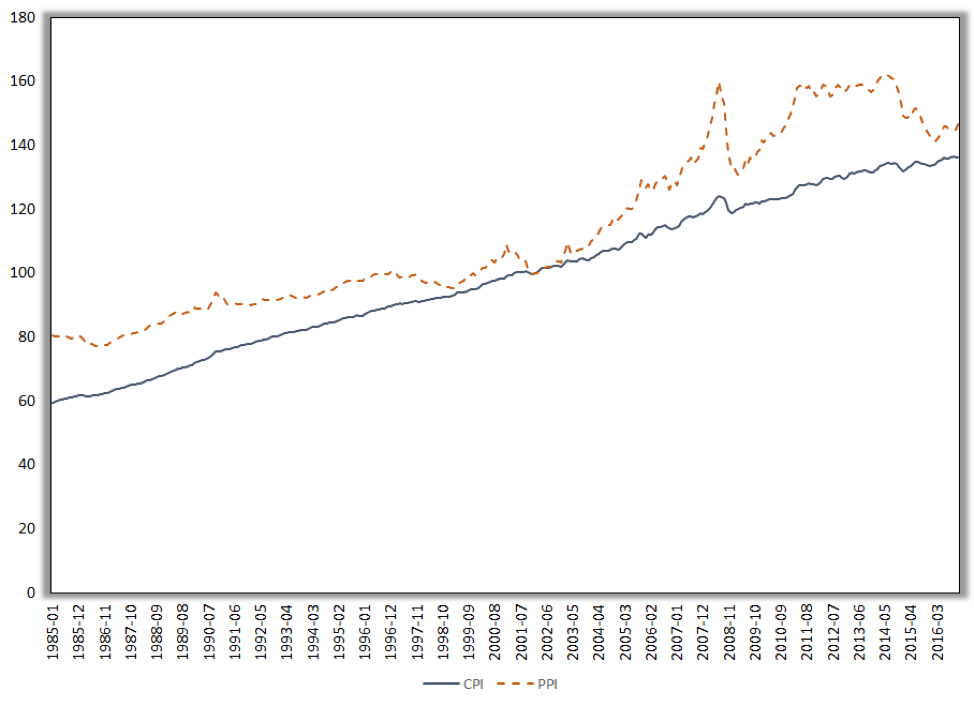

However, keeping the consumer price level stable in the presence of productivity gains does not mean inflation disappears. If the consumer price index is not allowed to fall, then the producer price index will increase. These two indices do not only show changes in relative prices. They can also point to a loose monetary policy even with a stable CPI. This is what we can see in the figure below.

The blue line shows the CPI, and the orange line shows the producer price index. Note that the CPI depicts a straight line, meaning inflation rates are fairly stable during this time period. The PPI, however, shows a higher rate of growth starting in late 2001 or early 2002. This suggests the Federal Reserve was misled by larger productivity gains. By aiming at price-level stability, it let money supply exceed money demand. Add to this the legal requirement for banks to increase mortgage lending, and the result is the blueprint for the housing bubble.

There is, however, a way for central banks to avoid these types of mistakes without having to estimate productivity gains in real time. As some have proposed since 2008, central banks should target a nominal income variable, such as nominal GDP. The advantage of this rule is that it allows the price level to move inversely to productivity gains.