You’ve probably heard it said that the Federal Reserve resorted to unconventional monetary policy to deal with the so-called Great Recession. Usually, discussions of the Fed’s unconventional monetary policy center on whether it has been effective. I’d like to consider a different angle: Was the Fed’s monetary policy unconventional?

To assess whether the Fed is doing something different, we must first understand what the Fed has traditionally done to conduct monetary policy. The Fed engages in open market operations—that is, it buys and sells assets from banks on the open market. When purchasing an asset, the Fed can create new money by either (1) ordering new notes from the Bureau of Engraving and Printing and paying banks in cash or (2) crediting the accounts of banks holding reserves at the Fed. In both cases, it is putting new money in circulation. In practice, it does the latter. When selling an asset, the Fed can destroy money by either (1) receiving payment in cash and destroying the payment or (2) debiting the accounts of banks holding reserves at the Fed. In both cases, it is taking money out of circulation. In practice, it does the latter. (Cash is taken out of circulation when it becomes too worn—but it is usually replaced with new notes.)

The Fed usually decides whether to expand or contract the money supply—and to what extent—be referencing its target. I’ve written recently about the federal funds rate target. Basically, the Fed expands the growth rate of money if the federal funds rate is above its target and slows the growth rate of money—or outright contracts the money supply should the growth rate be negative—if the federal funds rate is below its target. In principle, the Fed could target anything. Economists often consider price level targets, inflation targets, nominal income level targets, and nominal income growth targets in addition to federal funds rate targets. Perhaps we can consider these targets in another post as well as whether the target represents a binding rule which the Fed must follow or just a piece of information that the Fed should take into account when conducting discretionary monetary policy. As you might suspect, the devil is in the details.

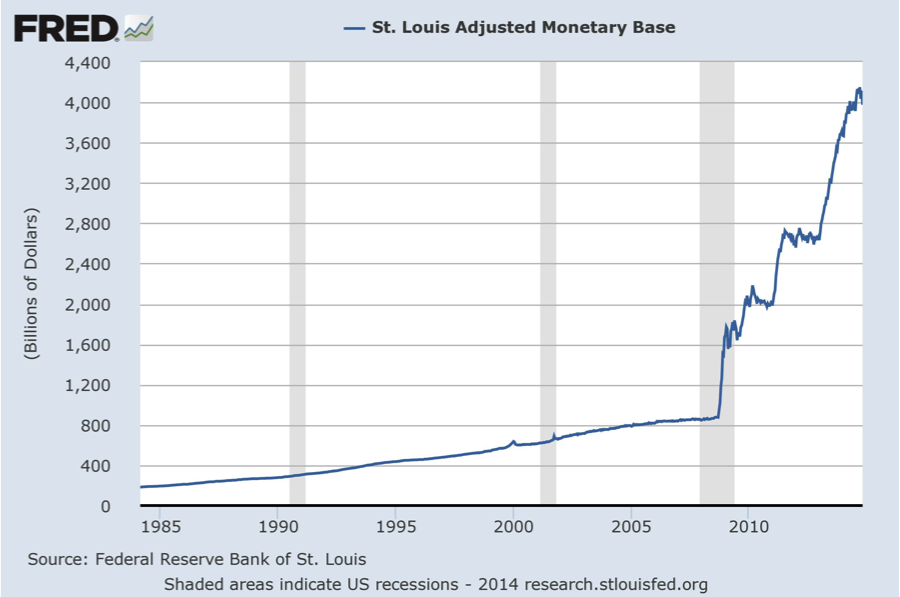

The monetary base—which includes currency and reserves held at the Fed—is shown in the figure below for the period 1984-02-15 to 2014-10-29.

It is clear from the chart that the Fed has presided over a massive expansion of the monetary base in recent years. But is this unconventional? On the one hand, it is just business as usual. The Fed expanded the monetary base by purchasing assets. It just purchased a lot of them. This isn’t unconventional so much as it is unprecedented. The Fed did what it does, only more so. In other ways, the Fed’s policy over the last few years has been unconventional. I will explain how it has been unconventional in my next blog post.