A common complaint about Bitcoin is its volatility. More than a third of all days, Bitcoin increases or decreases by 4 or 5 percent or more. This seems like quite a lot. And it is. The dollar increases or decreases relative to the euro by less than 0.4 percent on two-thirds of all days. And there was no day in 2018 when the exchange rate between the dollar and the euro changed by 1 percent or more. A 1 percent change would be a quiet day for Bitcoin. Gold, known as a speculative asset, varies quite a bit less than Bitcoin.

Some of this extraordinary volatility is due to news about Bitcoin. Despite its being almost a decade old, Bitcoin is relatively new; positive and negative developments naturally affect Bitcoin’s price and its prospects.

That said, it would be nice to be able to trace down a lot of that volatility to news. It can’t always be traced to news.

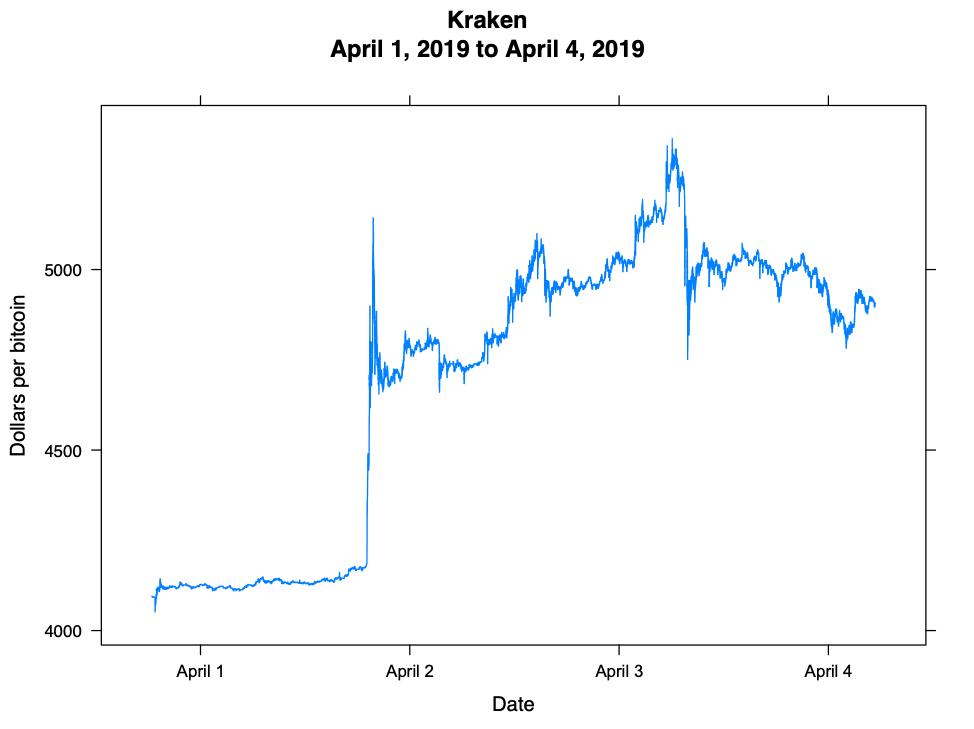

Bitcoin’s price increased substantially in April 2019. At the start of the year, Bitcoin was trading for about $3,900. By April 1, it was trading for about $4,150, only 6 percent more than at the start of the year. While Bitcoin had gone up and down, volatility seemed lower.

Then April arrived. Figure 1 shows the dollar price of Bitcoin on the Kraken exchange from April 1 to April 4. Kraken is a well-known exchange with a substantial amount of trading. There appears to be practically a straight shot up in the price early in the day on April 2. And prices on other exchanges show similar price increases.

Figure 1.

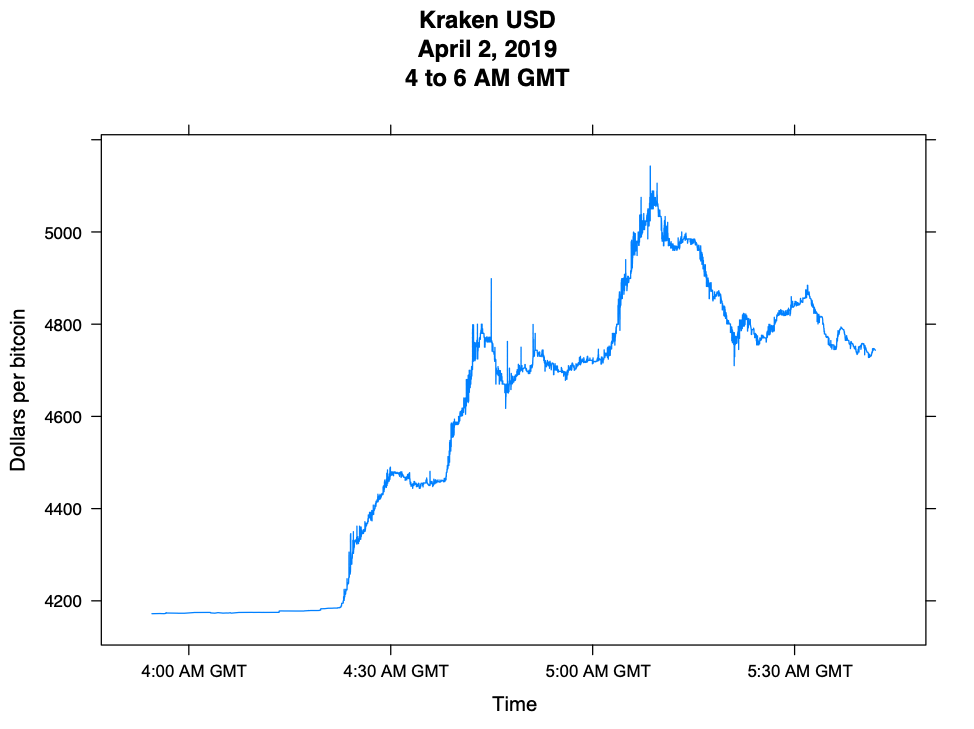

The date and time provided for the trades of the early morning of April 2 is the date and time in Greenwich, England. (Unlike stock exchanges, which trade during local business hours, Bitcoin exchanges trade 24/7. The convention for Bitcoin trades is to date trades as of Greenwich Mean Time (GMT) rather than where the exchange is located.) The price started to increase about 4:30 a.m. GMT. This is just before midnight on the previous day in the Eastern United States, evening on the West Coast, and about 1:30 p.m. on the same day in Tokyo. The increase may have been initiated in any of those places or anywhere else in the world. And the news may have appeared there or anywhere else in the world.

There was no obvious news, though, about Bitcoin on April 1. Rather than reflecting news after the information becomes publicly available, it is possible that prices increased because some people knew about a development before it was publicly available. There was no noticeable published news about Bitcoin on April 2 or even on later days. There was a lot of commentary about the price increase itself, but that is not helpful for finding independent news about Bitcoin.

It is possible that there was news about Bitcoin in some part of the world that was reflected in the price and never appeared in English. It doesn’t seem particularly likely, though.

There is commentary attempting to explain the increase (for example, see this CoinDesk article from April 30) based on past price and volume trends, which is called technical analysis. Technical analysis is of little value as a general rule, and its uselessness here is illustrated by the fact that these analysts somehow did not publish unambiguous forecasts of the increases before they happened.

Looking at the price in the early hours of April 2 provides a different perspective. Figure 2 shows the price from 4 a.m.to 6 a.m. GMT. The price did not increase in a straight line. Rather, the price rose a bit, then increased more, and finally increased more later over the course of an hour and a half.

Figure 2.

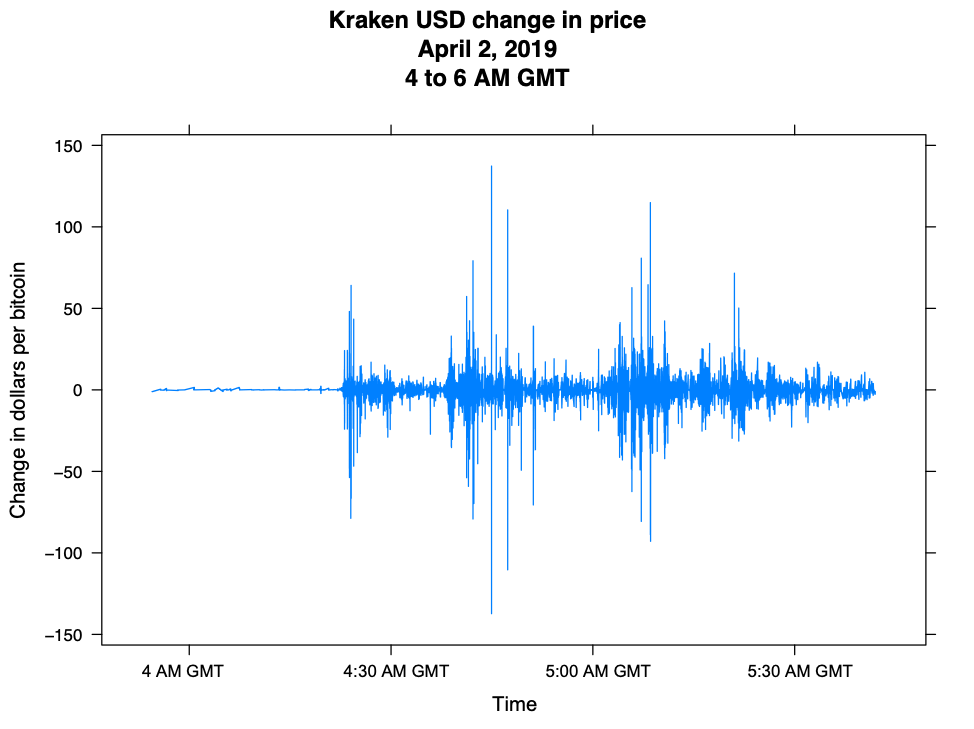

Volatility increased substantially. The increase in volatility is suggested by figure 2. Figure 3 shows the changes in the price over the same time period. The increase in volatility is dramatic. This pattern is reflected in United States dollar prices for Bitcoin on other exchanges and in other currencies’ prices for Bitcoin. Prices did not go straight up. Instead, prices rose and fell along the way to the increase by 6 AM GMT.

Figure 3.

Why didn’t the price rise right away? When asset prices on exchanges are responding to publicly available information, prices often rise as soon as the information is available. The increase in demand for Bitcoin apparently was not of that kind. It is more likely that someone or some group of people began buying Bitcoin, increasing demand and subsequently the price. The final effect on the price was not obvious. The effect on the price was revealed in the process of trading. In financial markets, this process is called “price discovery.” The process of trading itself reveals information about the price not known by any single buyer or seller. (This, of course, is related to a fundamental point made by Hayek years ago about information not available to individuals being revealed by prices in markets.) Why did the price increase? Demand increased, most likely because someone took a relatively large position. Based partly on information not available to the general public, BCB Group claims to have traced down the trades that initiated the increase. Bitcoin has seen people taking large positions before. It recently was revealed that one person, Masayoshi Son, lost $130 million on Bitcoin. Losing this much, even over the period when Bitcoin’s price fell from $17,000 to about $6,000 in months, required that Mr. Son acquire a big position relative to typical trading volumes. Many trades are for a fraction of a bitcoin now that bitcoin’s price is thousands of dollars instead of the pennies paid for a bitcoin when it started trading. There is an implication of this price increase for Bitcoin’s suitability as a store of value. As long as the price can increase by 20 percent — or decrease by 20 percent — while many people are in bed or going there shortly on the basis of no news whatsover, Bitcoin has zero chance of being seen as a reliable store of value. A highly speculative asset, maybe. But a reliable store of value, it is not.