When the Federal Reserve adopted an average inflation target in August 2020, I was cautiously optimistic. The period-by-period inflation target it had adopted in 2012 “does not anchor expectations very well,” I wrote at the time. Its new average inflation target, in contrast, should reduce the range of potential inflationary outcomes—and, hence, the risk of long-term contracting—by making up for past mistakes. “If credible and clearly articulated,” I wrote, “an average inflation targeting regime would provide a better anchor for inflation expectations than a period-by-period inflation targeting regime.”

Alas, it has not worked out so well in practice. Those caveats—that the average inflation target must be credible and clearly articulated—have proved to be crucial. Inflation has surged over the last year and, despite reaffirming its commitment to a 2-percent average inflation target on paper, the Fed’s own projections reveal it has no intention of making up for its past mistakes. Its failure to course correct risks unanchoring inflation expectations, leaving the Fed to choose between permanently higher inflation or temporarily higher unemployment.

Expectations, Risk, and Economic Growth

Since production takes place over time, people must form expectations about the value of the dollar in the future. Borrowers and lenders need to know how much future dollars will be worth when it is time to settle their loans. Employers and employees need to know how much future dollars will be worth when determining how much to offer and accept in long-term labor contracts. Business owners and their suppliers need to know how much future dollars will be worth when entering long-term purchase agreements. The nature of long-term contracting requires that we think seriously today about the future value of the dollar.

Unexpected inflation transfers real wealth from one party of a fixed nominal contract to another. Consider a simple lending agreement. If inflation is higher than was anticipated when the loan was entered, borrowers get to pay back their loans with—and lenders must receive—dollars that are less valuable than was expected. If inflation is less than was anticipated, lenders will gain at the expenses of borrowers. Borrowers and lenders will do their best to estimate the future value of the dollar. But there is some variance of potential outcomes. The greater the variance of potential outcomes, the riskier it is to engage in long-term contracts.

Monetary policymakers have the potential to reduce the inflation risk of long-term contracting—and the cost of estimating the future value of money—by reducing the range of potential outcomes for the price level. They can do this by (1) adopting a monetary rule that anchors inflation expectations and then (2) conducting monetary policy such that prices do not systematically deviate from that implied growth path of the price level. If market participants know how much inflation to expect, they do not need to incur unnecessary costs to estimate the likely course of prices. And, if the range of potential outcomes is narrow under the rule, they need not worry so much about the inflation risk of long-term contracting. By reducing the costs and risks of inflation, a good monetary rule increases productivity and, hence, promotes long-run economic growth.

Expectations and Average Inflation Targeting

In theory, an average inflation target can work well to anchor inflation expectations and reduce the range of potential outcomes for the price level. Consider a central bank that is committed to delivering 2-percent inflation on average. Monetary policy errors and unavoidable real supply disturbances will occasionally cause the central bank to miss its target. But the nature of the rule requires the central bank to make up for these misses.

Suppose, for example, that an unexpected monetary policy error causes prices to grow at an annualized rate of just 1.5 percent over the quarter. Wealth will have been transferred from borrowers to lenders and employers to employees over the period, as the dollars paid were worth more than was expected when they entered into their respective contracts. But the Fed can limit—and an average inflation target requires limiting—the extent of future errors by temporarily increasing the growth rate of money in this case such that prices return to the long-run growth path consistent with the average inflation target. In this way, the Fed reaffirms the expectations of those in long-term contracts.

An average inflation target also works reasonably well in response to temporary real supply shocks. Suppose, for example, that a temporary supply disturbance causes the price of oil to rise and, with it, the prices of goods and services in general. Inflation will temporarily rise, as prices exceed the long-run growth path consistent with the average inflation target. The central bank should not take steps to offset this rise in prices in this case, as potential output is reduced and prices should reflect the reduced production. However, oil prices will eventually decline (and, with them, the price of other goods and services) as supply disturbances ease up and production returns to normal. Hence, the initial above-target inflation will eventually be offset by a period of below-target inflation such that, over the long run, prices tend to grow along the path consistent with the average inflation target.

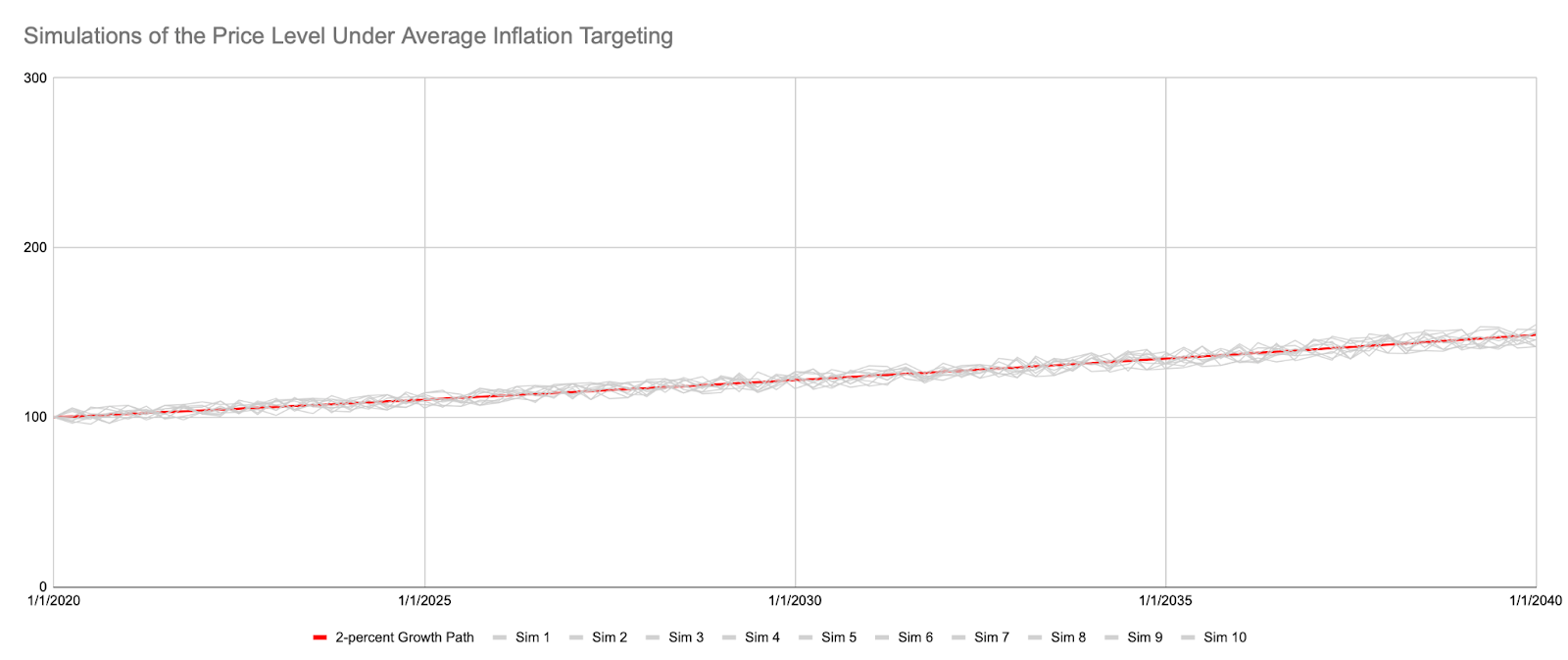

Figure 1 presents the results of ten simulations of the price level over a forty-year horizon when the central bank is committed to an average inflation target but occasionally errs in one direction or another. Note that the range of potential outcomes—and, hence, the inflation risk of long-term contracting—is relatively small. Again, that is because deviations from the 2-percent price level growth path are ultimately offset to ensure that inflation equals 2 percent on average.

Expectations and the Fed’s ‘Asymmetric’ Average Inflation Targeting

Unlike our hypothetical central bank, the Fed is not credibly committed to a clearly-articulated average inflation target. As Ricardo Reis notes in this excellent Twitter thread (and I have been saying for some time now), the Fed’s average inflation target falls short of the ideal in two ways. First, the Fed has not clearly articulated the period of time over which it will attempt to deliver an average inflation rate of 2 percent. Second, the Fed intends to let bygones be bygones, meaning it is not actually committed to delivering 2-percent inflation on average.

What is the Fed doing? David Beckworth argues that the Fed’s average inflation target is really an ‘asymmetric’ average inflation target. Under an asymmetric average inflation target, the Fed would take steps to offset shocks that push inflation below target but would not attempt to offset shocks that push inflation above target.

The idea that the Fed has actually adopted an asymmetric average inflation target would seem to conflict with a common sense reading of its Statement on Longer-Run Goals and Monetary Policy Strategy. Although it only explicitly states how it will respond to a shock that pushes inflation below its target, it seems to imply that the policy is symmetric. The reason the Fed has adopted its 2-percent average inflation target, after all, is to “anchor longer-term inflation expectations at this level.” In addition to being an abuse of the English language, an asymmetric average inflation target of 2 percent would not anchor longer-term inflation expectations at 2 percent. Rather, it would anchor expectations at some rate somewhat higher than 2 percent. It would also generate much more inflation risk in comparison with a conventional average inflation target.

I have repeated the same ten simulations presented above under the assumption that the central bank is committed to an asymmetric average inflation target of 2 percent in Figure 2. These simulations make two things clear. First, the variance of potential outcomes is much greater than that observed under a conventional average inflation target. Second, the expected rate of inflation—which can be estimated as the probability-weighted average across all possible simulations—is greater than 2 percent. Neither of these results are particularly surprising. If you have an asymmetric target, you should expect to get an asymmetric outcome.

The Federal Reserve has failed to adhere to the conventional average inflation target portrayed in its policy document. Either it has intentionally obscured the nature of its intended course of policy from the outset, by suggesting it would symmetrically target the average rate of inflation when it really intended to asymmetrically target the average rate of inflation, or it has abandoned its stated course of policy for an alternative that provides a much worse long-run nominal anchor. Neither of these two interpretations of the Fed’s recent actions bolsters its credibility.

A conventional average inflation target would have significantly improved upon the period-by-period inflation target the Fed adopted in 2012. It would have anchored expectations and reduced the inflation risk of long-term contracting, promoting economic growth in the process. An asymmetric average inflation target falls far short of that goal.