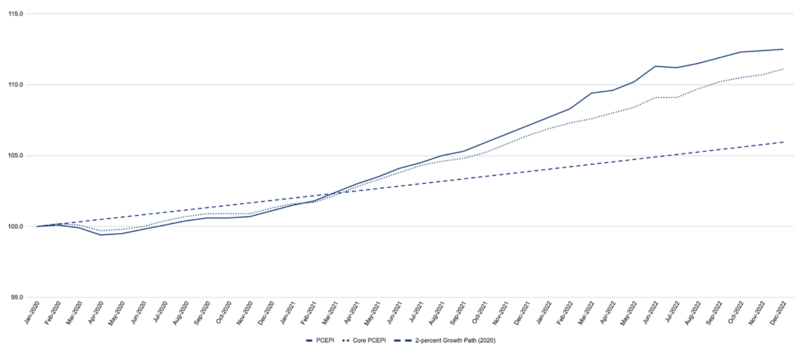

Inflation appears to be on the decline. The Personal Consumption Expenditures Price Index (PCEPI), which is the Federal Reserve’s preferred measure of inflation, grew at a continuously compounding annual rate of 4.9 percent from December 2021 to December 2022, down for the third consecutive month. Year-on-year inflation was a whopping 6.1 percent from September 2021 to September 2022.

Of course, the decline in inflation does not mean that prices are falling. It merely means that prices are not growing as fast as they were. The PCEPI is 6.6 percentage points higher today than it would have been had the Fed hit its 2 percent inflation target since January 2020, just prior to the pandemic. Moreover, Fed officials have indicated that they will not try to bring prices back down to the pre-pandemic growth path. In December, the median member of the Federal Open Market Committee (FOMC) projected 3.1 percent inflation for 2023.

Figure 1. Headline and Core Personal Consumption Expenditures Price Index, January 2020 to December 2022.

Although the 12-month inflation rate is certainly meaningful to households, some of which are struggling to pay the higher prices, it potentially obscures just how fast headline inflation is falling. The 12-month inflation rate is high, in part, because prices rose rapidly from December 2021 to October 2022. In the past two months, prices have risen at an annualized rate of just 1.1 percent, well below the Fed’s 2-percent target.

Fed officials are no doubt relieved to see inflation finally coming down, but they say they will keep working until the job is done. “Inflation is high, and it will take time and resolve to get it back down to 2 percent,” Fed Governor Lael Brainard told attendees at a recent event. “We are determined to stay the course.”

New York Fed President John Williams also said the Fed must “stay the course.” “With inflation still high and indications of continued supply-demand imbalances, it is clear that monetary policy still has more work to do to bring inflation down to our 2 percent goal on a sustained basis.”

Some Fed officials are prepared to go even further. In a recent speech, Dallas Fed President Lorie Logan said the FOMC will “need to remain flexible and raise rates further if changes in the economic outlook or financial conditions call for it.”

St. Louis Fed President James Bullard said he would prefer another 50-basis-point hike when the Fed meets next week, compared to the much-anticipated 25-basis-point hike.

The question now is whether headline inflation will remain low, or shoot back up in the coming months. “We don’t want to be head-faked,” Fed Governor Christopher Waller told attendees at an event last week.

Waller is right to be cautious. Although headline inflation has fallen considerably in recent months, core inflation—which excludes volatile food and energy prices and is thought to be a better predictor of future inflation—remains elevated. Core PCEPI grew at an annualized rate of 4.3 percent in December 2022. It had previously fallen from 3.3 percent in October to 2.2 percent in November.

It is hard to know how Fed officials are interpreting the latest inflation data. They have entered the blackout period ahead of next week’s FOMC meeting. At this point, it seems likely they will move forward with a 25-basis-point hike. But how high they will push rates this year, and how long they will keep rates high, remain open questions.